Weather is a uniquely interesting field because all of the tools we use to accurately forecast the future have improved over the last 50 years. And as you’d expect, our ability to predict the weather has similarly improved. Today’s 5-day forecasts are now equally as accurate as 1-day forecasts were 30 years ago.

I think most people imagine weather as one big system that passes through. Clouds roll in, it rains, it stops raining, the sky clears out. I’d guess if I told you to imagine a winter front coming in, you’d picture some big wide grey ceiling that lowers itself over a few hundred miles and lays down a blanket of snow. Meteorologists call this stratiform. Basically layer-cake weather, with everything underneath getting the same treatment.

But this isn’t the only type of weather pattern. If you’ve ever watched a thunderstorm form over the plains in the summer, it behaves quite differently. Instead what happens is you’ll get a single cell that builds (i.e. warm humid air at the ground rises into colder air above, the moisture condenses and you get these crazy localized cloud towers) and within an hour there’s hail/lightening/rain so heavy you can’t see 100 feet in front of you.

That cell matures, dumps its energy and then importantly, it dies. The downdraft (cold dense air falling out of the storm) fans out across the ground in every direction, moving as fast as 40mph and when it slams into the surrounding warm humid air that hasn’t stormed yet, it acts like a wedge that shoves the warm air upward.

If there’s enough instability in the atmosphere the wedge is exactly what’s needed to ignite the next storm cell, some ten or fifteen miles away from the first one.

The new cell was never going to form on its own. Sure, the energy was already loaded and waiting but what it needed was a trigger, which is exactly what the dying storm provides. Then the new cell just does the same thing.

When you string these cells together it forms what’s called a mesoscale convective system. From the ground you experience one storm at a time, each one feeling like the entire weather system. One side of you is dead calm, completely oblivious to what’s about to come, while the other side has already cleared out. If you looked at this from a satellite though, you’d see what looks more like a chain of events with a glowing line of separate cells, each at different phases of its life cycle walking across the plain until they run out of warm air to feast on.

What makes these types of chains possible and different from single storm fronts is a symptom of the conditions in the atmosphere. Specifically:

A boundary layer at the ground that is warm & wet (i.e. fuel)

Cold & dry air above that makes warm air want to rise into it (i.e. instability)

Winds at different altitudes blowing in different directions which gives the storms rotation to move sideways (i.e. shear)

When you get all three of these you get the procession-style storm I talked about.

Ok so why did I just talk about weather for 500 words?

I think the phenomenon described above is almost exactly what’s happened to financial markets today.

We used to live under a stratiform weather regime: one bull market, one bear market, slow rotations of leadership inside of it with a few years of each. We had a secular bull market from 1982 to 2000. A dot-com bubble after this. A housing and credit cycle from 2003 to 2007. These were all long, layered and mostly legible from the ground in such a way that you could be wrong about timing for years and still come out fine if you understood the regime.

That’s just not the world we live in anymore. Today we live under a convective chain regime: a procession of storm cells where each one feels total and unrelenting to whoever’s standing underneath it. Capital flows out of the dying narrative and ignites the next surge elsewhere (often in an adjacent area). The regime itself jumps from sector to sector on much shorter timescales that are measured in shorter & shorter time bands. AI infrastructure1. GLP-1s. Stablecoins. Quantum. Nuclear. DATs. Robotics. Space. Each of these has its own complete weather event with its own complete community of true believers, its own complete narrative arc and inevitably its own complete decompression. The cold downdraft then fans out and lights up the next cell a few miles away2.

It’s almost silly to pretend this isn’t the reality we live in. People love to poke fun at anyone who says “this time is different” but I think failing to acknowledge that the atmosphere of financial markets has shifted in a permanent way is either (i) intellectually lazy or (ii) a stubbornness of wanting the world to be one way rather than acknowledging the way it is.

Not Your Daddy’s Weather

For most of the post-war period, American financial markets ran like one very slow weather system. Bull markets lasted 10, 15, 20 years and sector leadership rotated within those secular trends.

The distinction here is that those rotations happened inside a coherent macro regime that only really flipped on specific generational pivot points.

The end of Bretton Woods. Volcker’s disinflation. The dot-com peak. The GFC.

I don’t necessarily think it’s a secret that there were structural conditions that made this the case. Trading was expensive3 which kept retail participation small and forced them to be patient. Pensions dominated household retirement4. The S&P 500 was a pretty balanced mix of manufacturing, energy, banks, retailers and a handful of media and tech names; the largest businesses produced earnings that grew with the economy in roughly linear and more predictable ways. Information also moved slowly. The gap between a 10-K filing and most investors knowing what was in it was measured in weeks.

At the same time, volatility was more symmetric. Bull markets had real corrections with drawdowns that flushed out leverage and reset positioning over longer periods of time. We didn’t see nearly the same degree of these kind of violent sell-offs and V-bottoms. Bear markets similarly had real rallies that took time to play out. The market frequently spent meaningful time at different levels of agitation and ~generally~ the transitions between regimes were measured in quarters or years.

If we revisit the atmosphere analogy: there was modest fuel, moderate instability and low shear. Broad, slow, layered weather that you could plan around. Every one of those conditions has now shifted with several actually inverting, and the result is a structural transformation of the conditions themselves.

What Changed?

A lot of these shifts ultimately overlap and amplify each other but tbh I think each has independently been large enough to reshape markets. Taken together they explain a lot of what has taken many smart people a long time to digest (some still haven’t, we will get to them later).

I count 8.

The democratization of the speculator class

The infinite bid

Passive investing & the inelastic counterparty

Pod shops, HFTs & the hollowing of the middle

Volatility suppression

Composition mix

The collapse of information lag

Fiscal & monetary regime change

The democratization of the speculator class

These aren’t necessarily in order of importance but top of mind for me lately has been the undeniable shift of who is actually in the market. In the 1990s retail accounted for ~10% of US equity volume. There’s a lot of reasons for this but most retail investors held individual stocks for years and if they ever traded it was through full-service brokers who charged commissions that made anything resembling active speculation pretty prohibitive. Robinhood famously introduced zero commission trading and pioneered the payment-for-order-flow model that made the economics work. But even that has been misremembered a bit because Schwab didn’t cut its commission to zero until the fall of 2019, and this was the real domino because we saw Fidelity, TD Ameritrade & E*Trade all follow suit within weeks.

Obviously the pandemic accelerated the trend: stimmy checks, bored people stuck at home, mobile-first trading apps that were intentionally designed to gamify the experience. Retail share of US equity volume jumped to 25% in 2020-21; even in the moment a lot of people thought this was a temporary blip but it’s stayed elevated ever since. JPMorgan reported a record 48% of total order flow on April 29th last year during the tariff-driven volatility spike. On a normal day now, retail runs more than double its pre-2020 share and on especially volatile days they can extend to as high as 35% of volume.

A related and perhaps deeper shift is what retail actually trades. Single-name options have become their expression of choice and we all know the insane explosion of 0DTEs. The marginal new participant is younger, more concentrated, more thematic and maybe(?) most importantly both (i) more leveraged in convex ways that don’t show up in margin debt statistics & (ii) far more reactive to price action than to fundamentals. They’re also way more likely to be tailing someone else5.

A boundary layer at the ground that is warm & wet (i.e. fuel)

The boundary layer is wetter and hotter than it’s ever been meaning the potential energy at the ground swells in a way that it never did before.

The Infinite Bid

This particular shift is one I’ve written about in the past. For more context you can read that blog but the TLDR is that US retirement plans have shifted from defined-benefit pension plans to defined contribution ones. The individual for better or worse is now responsible for their own retirement in a way they weren’t historically. At the market level this just means that every pay period, there’s a huge, mechanical, price-insensitive bid for equities. It’s autopilot flow.

Pensions didn’t work like this because defined-benefit pensions were managed against liabilities, which means managing duration risk. In practice, this meant that the people managing pension plans had to decide at times that “hey equities look expensive here, we should shift the mix toward bonds”. Even if the flows were slow here, they were still more active than the passive infinite bid we see today.

Why this matters is because we’re mostly interested in understanding what the marginal active dollar is doing and today’s marginal dollar has more leverage on price-setting than it did in the past.

Passive investing and the inelastic counterparty

Passive investing by construction is an inelastic counterparty in the sense that it doesn’t care about price. It buys the index in proportion to weight, full stop. As a stock gets larger, passive buys more of it and visa-versa. The weird thing about this construction is that it sort of embeds momentum as infrastructure. The things working best get the largest mechanical bid moving forward and this is at least party how we end up with the Mag7 phenomenon6.

Plenty of people have written a lot about the concentration at the top of the indices and how much it has swelled over the last decade7. But I don’t know that the concentration is necessarily unjustified —8 the point is that passive flows don’t really have a natural off-switch.

Pod shops, HFTs & the hollowing of the middle

So the market has introduced a permanent passive price insensitive bid. At the same time we’ve seen the active layer transform in important ways, the defining structural change being the rise of the multi-strat pod shop. Citadel, Millennium, Point72, Balyasny, etc. These places house hundreds of independent PMs who each run a specialized strategy and operate on strict, tight risk leashes. AUM growth for these entities has been hilarious and honestly, capital is concentrating in the top names here in the same way it has at the equity index level.

Combine this with the fact that HFTs now account for anywhere between 50-60% of US equity trading volume and as much as 75% of futures volume, and you get a uniquely fragile environment. Intermediaries trading with themselves aren’t functioning as any sort of price discovery mechanism so a lot of the “volume” we see on the tape is just plumbing. The ultimate effect of this dynamic is that you get extremely tight spreads in normal conditions, which is obviously a good thing. But when something actually moves, i.e. a narrative cracks or positioning has built up too far in one direction or when a pod shops’ risk limits start tripping in correlated ways9, the microstructure basically gets out of the way. Pod shop structure makes this worse in a very specific way because every PM at every platform is running the same factor exposures, has the same drawdown limits and so when one team is forced to de-gross so does everybody else. February 2018. August 2019. March 2020. August 2024. These will keep happening because the structure that produces them is now baked into the financial system.

In a lot of ways the guys who got squeezed out in this world are the traditional fundamental L/S managers who have some theses, a 20-40 name book and multi-quarter time horizons. That model got pushed either up into the platforms or drifted sideways into private markets, family offices or concentrated single-strat funds. I’m biased but there is likely meaningful alpha to be generated by understanding the narrative shifts and having the patience to sit between marginal new flow and the marginal new exit.

Volatility Suppression

Ok so we’ve got these 4 ingredients:

how wet boundary layer (democratizing speculative class)

perpetual passive bid

inelastic passive counterparty

pod-shop microstructure with synchronized risk discipline

Now the volatility regime almost has to look the way it does today. Empirically we know the VIX spends most of its time at low levels: somewhere around 2/3 of trading days since 1990 have closed with a VIX below 20. Day-to-day autocorrelation of VIX is up to ~85% meaning that today’s vol looks almost exactly like yesterday’s. But the transitions are now violent and asymmetric. There are studies that suggest most of the vol explosion happens in the days immediately following a compression break (duh!) but that the decay back downwards takes much longer and is spread over a handful of weeks.

There are some structural reasons for this: a huge industry now exists for selling vol10. But inevitably tail risk shows up and everyone unwinds all at once. The 0DTE proliferation makes this even more complicated because dealer hedging of these products create gamma profiles that further suppress intraday volatility.

This was a lot of words that really just say the distribution of vol has gotten worse. So the market is spending more time in compression phases and then pays for that with bigger, more violent releases.

Composition mix

The sixth shift is the actual composition of the market. In 1980 the S&P 500 was a manufacturing heavy index. Industrials, materials, energy, financials and consumer staples were the bulk of it. These companies produced earnings that grew at roughly the rate of GDP and roughly in linear ways, which meant it could be valued with roughly mean-reverting multiples. Estimating the 5-year forward earnings of Proctor & Gamble was not exactly something you could be orders of magnitude off on.

Compare that to today…

Information Technology + Communications Services + some of the tech-adjacent slices of Consumer Discretionary (Amazon, Tesla) sit above 40% of the S&P 500. Many of these companies don’t operate on linear economics. Software famously was lauded for having near-zero marginal cost of distribution and AI is even more of a Rorschach test: AI labs are either enormous capex sinks that turn into the most valuable economic infrastructure of the next half-century or they’re some kind of delusional money pit, doomed for disaster. Estimating short-term earnings is difficult enough for these companies, let alone terminal value math where uncertainty is highest and prone to the most violent swings in valuation. In many ways these companies have shifted from P&L exercises to narrative ones. Again, this means there’s alpha for investors who can take a view on the trajectory of a frontier technology, the durability of emerging (and existing) moats and the shape of markets that don’t really exist yet.

Widget factories used to add capacity in linear chunks and so discounting cash flow models mostly converged on reasonably stable estimates. Multiples mean-reverted far more often in that paradigm. Today, an increasing share of today’s multiples is a function of how much investors believe the story being told. And for what it’s worth I don’t actually think this means valuation frameworks are broken but it’s kind of just the reality of the types of companies that exist in 2026.

The new financial market indices are full of these long-duration, narrative-driven businesses. Each of these has a much steeper lapse rate11. The steeper the gradient, the more potential energy is locked in the system and by extension the more violently that energy converts to motion when something triggers it.

The collapse of information lag

Everyone has lived through this in some ways and probably intuitively understands it so it’s perhaps less interesting but also maybe now under-appreciated. Throughout most of financial history any kind of market-relevant information was rate-limited by some speed-of-publication bottleneck. Today information latency is literally zero.

Positioning information in particular seems to propagate faster than anything as investors immediately see how every “smart” person they respect reacts to news in real-time (more than ever a lot of people are disclosing positions as well). Part of this onslaught of real-time information is that there’s a constant buzz of comparison under the surface. PnL screenshots are everywhere, stories of someone turning $1K into $5M regularly go viral. There’s a permanent engine of FOMO roaring louder every day.

Fiscal & monetary regime change

I actually don’t think this needs to be explained in detail at this point. So the cliff notes are

US monetary policy structurally easy with real rates near zero for a long time

QE expanding Fed balance sheet by trillions

Every duration-sensitive asset traded at a premium with the discount rate so low

Then fiscal added to this with stimmy checks, PPP, Inflation Reduction Act, CHIPS Act

War-time deficits while at full employment

K-shaped economy dynamic as stimulating financial markets & stimulating main street economy are very different things

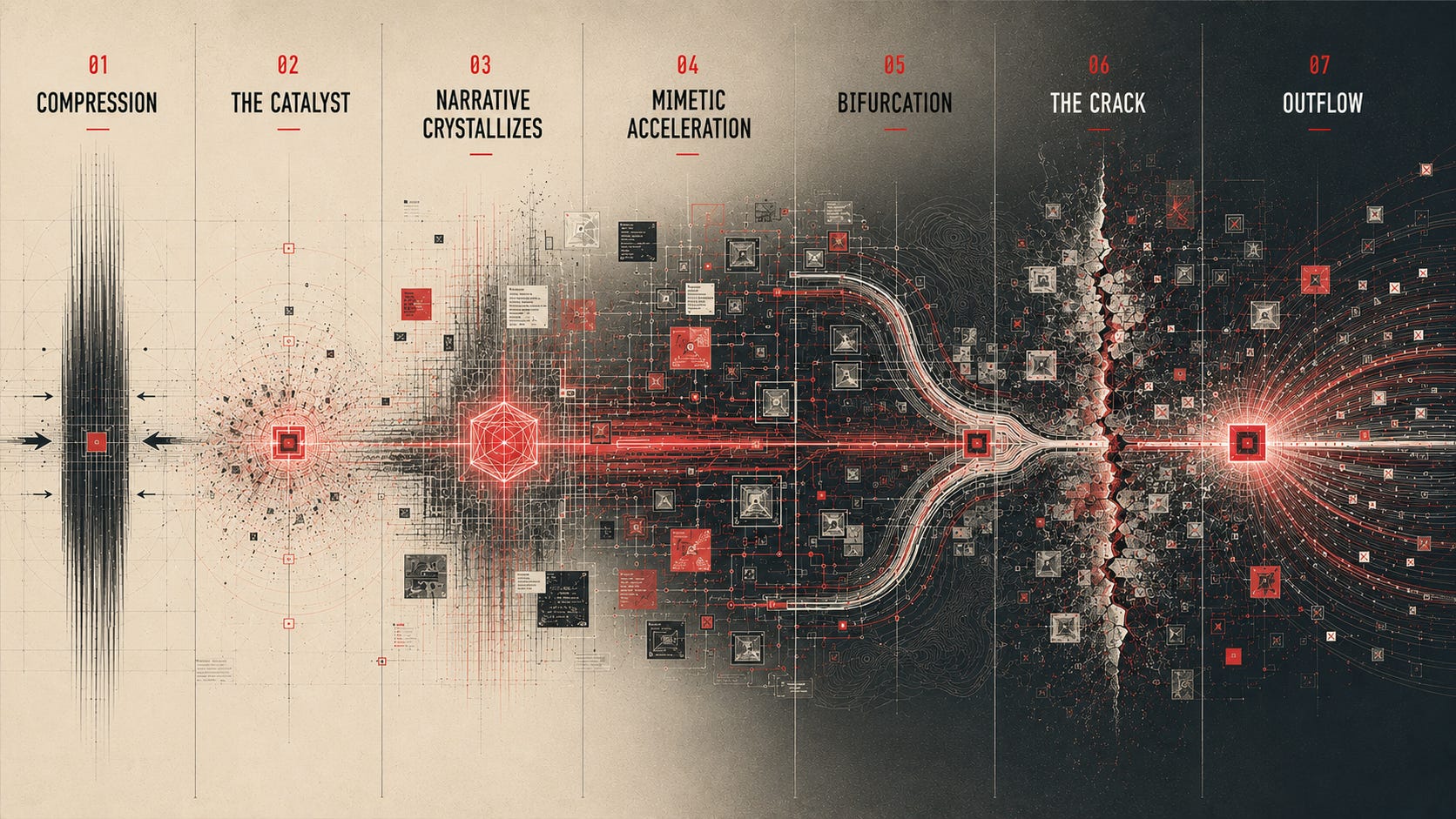

How The Storm Forms

It’s much easier given all the above to now visualize how these rolling bubbles become inevitable.

I won’t go through all these stages individually because they’re reasonably self-explanatory but let me call some things out.

The compression stage is something we’ve uniquely seen at Compound investing across a bunch of (seemingly) disparate areas for a long time. Categories/sectors/industries come in and out of favor all the time and with that comes a lack of attention and interest. But there are always talented people building regardless of the outside perception and the reality is that most of the time they’re not going to be in the spotlight.

Eventually some legitimate change happens that brings the interest back around, be that a real technological breakthrough, a regulatory shift, an earnings surprise that changes the scale of the underlying business reality. The domain specialists will should notice this first.

At some point the narrative is crystallized (aka the story gets a name) which does a few things, one of which is that it flattens what’s actually happening. Some people find this annoying because they hate meme’s or think it’s bastardizing something they hold dear but the reality is this makes the narrative easier to understand (and importantly share). It becomes way more legible to a broader audience who can’t necessarily evaluate the entirety of it on merit alone (even with LLM help).

At some point you reach a stage where we see bifurcation. The modern context of this is that the marginal buyer outside of “the believer cohort” shrinks to zero. You reach a point where the valuation gap between believers and skeptics becomes too large such that even those people chasing the narrative fall off as marginal buyers.

The crack is always obvious in hindsight, though in 2026 people are way too quick to try to call this ahead of time. This again is just the reality of the hyper-online, comparison, clout-chasing world we live in. But this crack gives way to the de-grossing as factor exposure unwinds for everyone and the outflow then goes searching for a new pocket of warm humid air to trigger a new cell.

Future Forecast

The downstream effects of this regime are significant. And I think this is more an acknowledgment that the shape of the weather is in theory more predictable without necessarily knowing the exact location of any given storm.

Ok but what does this mean about the future?

Well one argument that a lot of people made just after COVID was that “this is an anomaly” or “[redacted] was a zero interest rate phenomenon”. Some of this was obviously true. But to me it’s become more clear that the broader regime shift is permanent. How permanent is a debate for another day. But each of the shifts I described above is pretty one-directional…

trading commissions are not going back up

passive investing doesn’t just unwind

defined-benefit pensions are gone forever

social media isn’t going to get slower in the future

pod shops — maybe these dissolve quicker than I appreciate but given the parabolic growth and how much money they’re making that seems unlikely

information lag isn’t going to lengthen

You can almost think of these conditions as the new climate we live in. Candidly, I think anyone expecting us to return to the previous stratiform regime of the 80s or 90s is just in denial.

Another claim that’s maybe(?) finding some kind of local maxima is the idea that these rolling bubbles will keep compressing in duration. This is one of those things that I think is tougher to say just because it turns into a never-ending meta game of “i know that you know that i know that you know…”. But the simplest lesson is that each cycle teaches participants what the pattern looks like which in theory speeds up the next one. Crypto participants now feel comfortable trading tradfi assets because many of the survivors there have so many reps already with these types of behaviors. And while I don’t necessarily subscribe to the idea that crypto traders are best suited for this new world, I understand the argument. Some probably are. To me though, there is some half-life of narrative-driven markets that can only be compressed so much.

Maybe the most critical claim I’ll make about what the implications are is that this new rolling bubble world rewards a couple types of investors. Domain specialists who actually understand what would need to be true for the narrative to deliver on its priced-in promises (or exceed them). But this means understanding true technical bottlenecks, regulatory nuance, manufacturing supply chain dependencies, competitive dynamics all the way down to unit economics. Realistically this is not where most people will sit. I think AI models probably make people believe they live in this category more than they do, which is especially dangerous12. The reality is most actually sit in an adjacent seat where they are trying to understand how the next-most-informed participant will react. There’s probably a completely separate piece on why the combination of these two is likely to become an even more rare trait over the years but this blog is already long enough.

One thing that’s clear is we are certainly not at a loss for future narratives:

AI infrastructure & applications

Robotics

Physical AI

Precision medicine

Crypto

Materials science

Fusion, advanced fission, grid storage

Space

BCI

Quantum

Even within these we’ll see ripples form and dissipate as investors move up and down the supply chain and tech stack within these.

Retail’s biggest advantages in financial markets have always been time and flexibility. That is to say, they don’t need a few days to schedule investment committee decisions, or convene on allocation sizing. They also aren’t beholden to the same shorter-term pressure that many institutional managers face (i.e. there’s no quarterly redemption in your PA). This may explain some of the outperformance retail has enjoyed. Decades of BTFD working also probably helps. So in some sense, retail participants who have the ability to manage risk are in a great position.

The View From Above

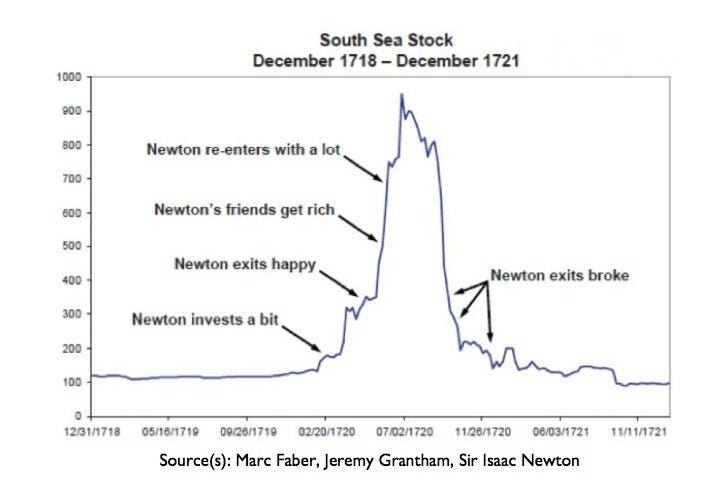

A lot of what I’ve (too verbosely) written above may leave the impression that I care one way or another about the things that have led us to the market structure we have today. Sure I have opinions on some of those things. And when investing on the private side, I still think there are plenty of ways to make money without funding things that accelerate net-bad societal outcomes. But one of the most common mistakes a lot of people make in public markets is making decisions based on how they want the world to be13. I get this. We’re all humans with emotional triggers that have been hard-coded into our DNA for centuries. It’s why Newton re-entered with a lot.

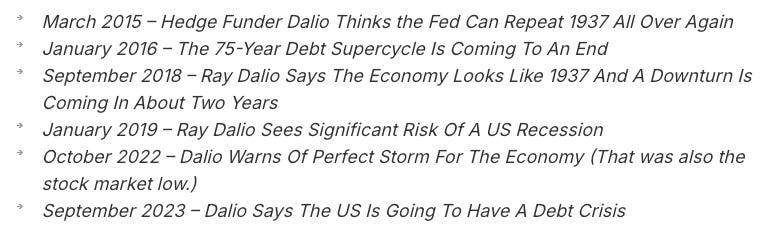

But it’s a huge barrier to performance. For years we’ve seen asset managers and hedge fund guys come on TV and talk about why markets are wrong or wax poetic about impending recessions. Much like our friend Sisyphus, these guys do not come on TV for charitable purposes. Ray Dalio has been calling for a debt crash the entirety of this historic bull market.

The world is not going back to your father’s market. Is this convective regime a more degenerate version of the old stratiform one? I’m not actually sure to be honest. Potentially? But at the same time a lot of the shifts that are producing it I actually think are net-good things: democratized access14, automated retirement saving, passive ownership, more real-time information. All of these things reflect a market that is way more available to ordinary people than it was in the past.

An aside that I tweeted about the other day (there’s a more philosophical piece to be written here):

From the ground, every storm is total. The world narrows to whatever is happening to you right now. This is the experience of market participants in any of these sector cycles. On the ground, it feels like a black hole of liquidity sucking up everything around it. Only if you are able to step back and move to altitude are you able to actually see the chain. One cell after another lighting up. Each of them at different phases and each of them feeling total and complete to the people underneath them.

Markets are so intoxicating because they are simultaneously always changing and yet, at least today, the humans still have control over price discovery. And humans are inherently emotional beings that can’t help but make the same mistakes over and over. That tension helps create the conditions we experience each day, which ~feels~ quite frenetic in the moment but taking a step back looks a lot more like rolling bubbles.

Really the point of all this is to try to drift above the immediate storm and operate at a higher system level to allow yourself space to recognize which way the front is moving, and to detach yourself as much as possible from the immediate sensory-overload effects of any individual cell underneath.

As with most things that require immense discipline, this is simple but not easy.

hope you enjoyed, thanks as always for reading semi-lucid thoughts. if you want more feel free to sub, it’s free

which within itself has its own rolling narratives

one of the funniest things about this is seeing people on twitter say things like “nobody is even talking about xyz yet” and it’s an entire massive sector that has tons of people talking about it they just don’t happen to overlap at all with this random narrative trader

a round-trip stock trade through a full-service broker cost roughly the equivalent of a steak dinner in real terms

in 1980 almost ⅔ of private retirement contributions still went to defined-benefit plans which meant most of the wealth being saved for retirement was deployed by professional fiduciaries operating on multi-decade liability horizons

obviously these companies are also exceptional at making money and growing earnings

there is some truth to it but i also think it’s not necessarily that fair to think of some of these companies as 1 company

guy who thinks you’re not allowed to use em dashes anymore bc AI’s corrupted it

btw these guys are in all the same trades

covered call ETFs are a massive category, dispersion trades (short index vol, long single-name vol) are a core book at every multi-strat, structured products from banks systematically harvest premium. all of these things just manufacture the calm by collecting income in exchange for taking tail risk

the steepness of the temperature gradient between the surface and the upper atmosphere is the lapse rate

fwiw robinhood is one of my least favorite companies in the world. i think the fact that they pretend they’re helping people on some type of financial journey but in fact design the entire company/product around turning their users into degenerate gamblers is gross.